Europe Greenhouse Horticulture Market Size

The greenhouse horticulture market in Europe was valued at USD 11.59 billion in 2024 and is anticipated to reach USD 12.54 billion in 2025 from USD 23.48 billion by 2033, growing at a CAGR of 8.16% during the forecast period from 2025 to 2033.

Greenhouse horticulture refers to the controlled-environment cultivation of high-value crops within engineered glass or plastic-covered structures designed to optimize light, temperature, humidity, and nutrient delivery. It is primarily for vegetables, fruits, and ornamental plants. This agricultural model enables year-round production independent of external climatic fluctuations, enhancing food security and resource efficiency. As per a study, hectares of land across the European Union were dedicated to protected horticulture, with the Netherlands, Spain, Italy, and France accounting for a portion of this area. As per the European Environment Agency, modern greenhouses consume 30–50% less water than open-field farming due to closed-loop irrigation systems. Apart from these, according to the study, greenhouse-grown tomatoes in Northern Europe achieve a higher yield per hectare compared to field cultivation, which emphasizes the sector’s agronomic efficiency and strategic importance in sustainable food systems.

MARKET DRIVERS

The intensifying demand for locally grown and pesticide-reduced produce, particularly in urbanized regions where food traceability and freshness are prioritized, is boosting the growth rate of the Europe greenhouse horticulture market. Consumers across Western and Northern Europe increasingly favor vegetables and herbs cultivated in controlled environments due to their lower chemical residue levels and reduced environmental footprint. According to a November 2023 survey by BEUC and the International Consumer Research & Testing (ICRT) network, only two in five (40%) of European respondents said they would be willing to pay more for a product bearing a verified environmental label. Furthermore, as per the research, a portion of tomato and cucumber production in the Netherlands now occurs in integrated pest management (IPM)-compliant greenhouses, utilizing biological controls such as predatory mites, thereby meeting stringent EU pesticide reduction targets under the Farm to Fork Strategy.

Integrating greenhouse horticulture into urban and peri-urban food systems accelerates the pace of expansion of the Europe greenhouse horticulture market. This integration is driven by the need to shorten supply chains and reduce transportation-related emissions. Cities such as Copenhagen, Paris, and Rotterdam are actively supporting the development of commercial-scale greenhouse complexes on the urban fringe to enhance food resilience. As per the study, urban and peri-urban agriculture now contributes to a portion of fresh vegetable consumption in major European metropolitan areas. In addition, the City of Paris launched an initiative to convert hectares of underutilized land into high-tech greenhouses by 2030, aiming to supply a portion of the city’s fresh produce locally. This spatial reconfiguration of food production is increasingly supported by municipal policies and EU cohesion funding, which strengthens greenhouse horticulture as a cornerstone of sustainable urbanization.

MARKET RESTRAINTS

The high capital intensity and energy dependency of climate-controlled facilities, particularly in colder Northern and Central European regions, is a significant obstacle impeding the growth of Europe’s greenhouse horticulture market. Maintaining optimal growing conditions during winter months requires substantial heating, lighting, and ventilation, which leads to significant operational costs. According to a study, natural gas prices for agricultural producers in the EU surged, forcing many greenhouse operators to reduce cultivation cycles or scale back production. Apart from these, according to research, a standard hectare of heated glasshouse in Germany consumes notable m³ of natural gas annually, which makes energy volatility an important vulnerability for long-term investment and profitability in the sector.

The scarcity of skilled labor and technical expertise required to operate advanced greenhouse systems, which rely on complex automation, data analytics, and integrated crop management, poses a substantial challenge to the Europe greenhouse horticulture market. As per the study, the horticulture sector faces a deficit in qualified technicians capable of managing climate computers, hydroponic systems, and IPM protocols. In the Netherlands, despite being a technological leader, a portion of greenhouse operators reported difficulty in recruiting staff with dual competencies in agronomy and digital systems, according to a study. This skills gap is exacerbated by an aging workforce. Hence, a lack of targeted training and immigration policies for agri-tech talent risks sector stagnation since next-generation greenhouses demand higher cognitive and technical input compared to traditional farming models.

MARKET OPPORTUNITIES

The deployment of renewable energy integration within greenhouse complexes, enabling energy self-sufficiency and compliance with EU decarbonization mandates, offers new opportunities for the Europe greenhouse horticulture market. Solar photovoltaic (PV) panels, geothermal heating, and biomass cogeneration are increasingly being adopted to power climate control systems. According to the research, many commercial greenhouses in Europe have installed on-site solar arrays, collectively generating GWh annually. Furthermore, as per the study, greenhouse farms using straw-based combined heat and power (CHP) systems reduced CO₂ emissions compared to gas-heated units. Hence, such energy innovations position greenhouse horticulture as a scalable model for climate-resilient agriculture.

The adoption of artificial intelligence and digital twin technologies to optimize crop performance and resource efficiency is giving rise to new opportunities for the growth of Europe’s greenhouse horticulture market. AI-driven platforms analyze real-time data from sensors monitoring light, CO₂, humidity, and plant physiology to adjust growing parameters autonomously. As per the study, AI implementation in Dutch tomato greenhouses can improve yield uniformity and reduce water usage. Companies have developed cloud-based decision-support systems used across hectares of European greenhouses. Apart from these, the European Commission’s Horizon Europe program has funded projects focused on digital twins, virtual replicas of greenhouse environments, that simulate crop responses to different inputs. These advancements are redefining precision horticulture, which offers unprecedented control and scalability.

MARKET CHALLENGES

The fragmented regulatory landscape governing water use, emissions, and plant protection products is a primary factor that challenges the Europe greenhouse horticulture market. This complicates compliance for cross-border operators. The EU sets overarching environmental directives. But, national and regional authorities implement varying thresholds for nutrient discharge, CO₂ enrichment, and pesticide residues. According to the study, different regulatory frameworks govern greenhouse wastewater reuse across EU member states, creating administrative burdens. The European Committee of Farmers’ Associations emphasized that inconsistent enforcement of the Sustainable Use Directive leads to competitive imbalances, particularly disadvantaging smaller producers who lack legal and technical advisory resources, which impedes the sector’s harmonized development.

The vulnerability of greenhouse infrastructure to extreme weather events linked to climate change, including prolonged heatwaves, hailstorms, and heavy snowfall, is degrading the Europe greenhouse horticulture market. Structural damage from climatic anomalies can lead to catastrophic crop loss despite greenhouses being designed for environmental control. As per the research, the frequency of severe weather incidents affecting agriculture increased. Existing greenhouse designs may require costly retrofitting with adaptive features like dynamic shading, strengthened glazing, and emergency cooling systems to ensure long-term operational resiliency, especially as climate projections indicate intensified weather volatility in Mediterranean regions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.16% |

|

Segments Covered |

By Covering Material, Application, Product, and Country |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Richel Group, Hoogendoorn Growth Management B V, Certhon Inc, Dalsem Horticulture Projects B V, HortiMaX B V, Harnois Greenhouses, Priva B V, Ceres Greenhouse Solutions, Certhon, Van Der Hoeven, Oritech Solutions, Netafim Ltd, Ridder Holding Harderwijk B V, Rough Brothers Inc, Top Greenhouses Ltd, and others. |

SEGMENTAL ANALYSIS

By Covering Material Insights

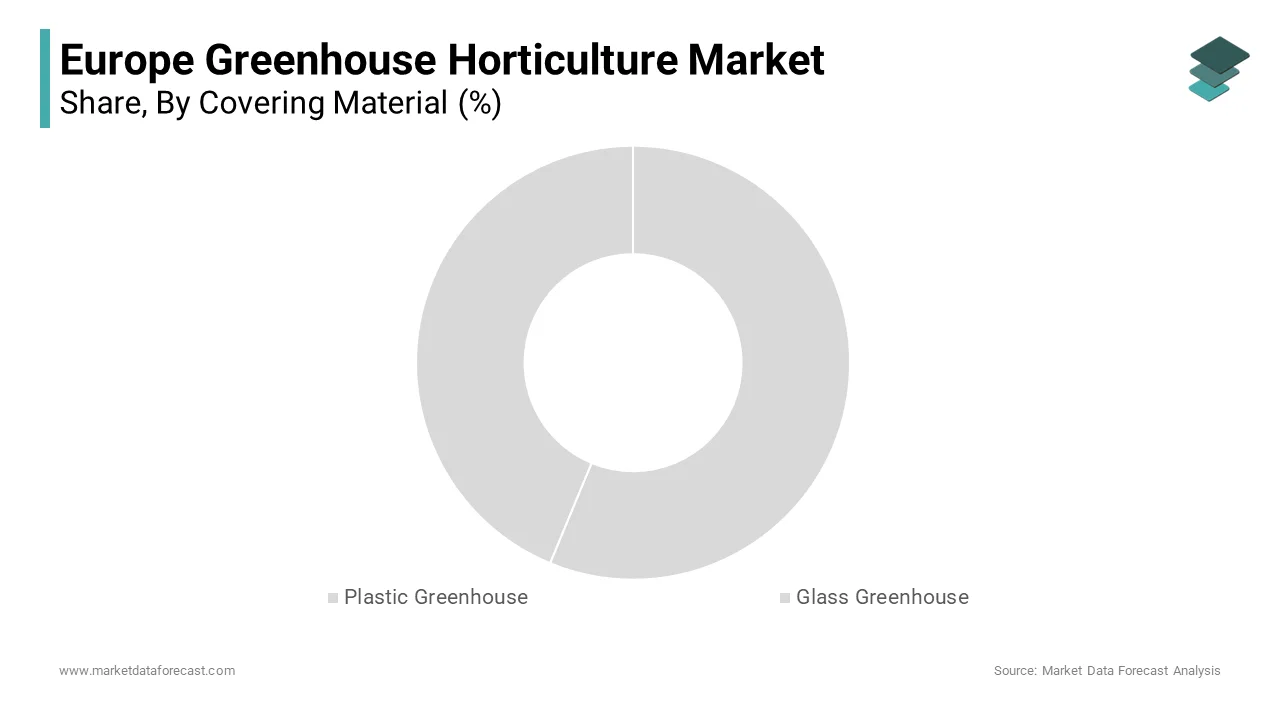

The plastic greenhouse segment dominated the Europe greenhouse horticulture market by accounting for 58.2% of the regional market share in 2024. The material’s cost-effectiveness and rapid deployability, particularly among small and mid-sized growers, are primarily driving the growth of the plastic greenhouse segment in the regional market. Polyethylene (PE) and polyvinyl chloride (PVC) films are widely used due to their low initial investment. In Eastern Europe, where capital constraints are more pronounced, plastic greenhouses constitute a portion of protected cultivation, as per the study. Apart from these, according to research, plastic tunnels enable seasonal extension in temperate zones, increasing vegetable harvest windows, which makes them indispensable for early-season crop production in countries like Romania and Bulgaria. Continuous innovation in multilayer film technology, enhancing durability, light diffusion, and thermal retention, also propels the rise of this segment.

The glass greenhouse segment is predicted to witness the highest CAGR of 9.3% from 2025 to 2033 due to the increasing deployment of energy-efficient, climate-smart glasshouses in Northern and Central Europe, where year-round production demands superior insulation and structural resilience. Modern glass greenhouses utilize double-glazed, low-emissivity (low-E) panels that retain more heat than traditional single-pane structures, as per the study. Rapid growth is its integration with district heating and circular energy systems is a further accelerator to the expansion of this segment in the regional market. In Denmark and Sweden, municipal waste-to-energy plants now supply residual heat to commercial glasshouses, drastically reducing reliance on fossil fuels. These synergies with urban energy infrastructure make glasshouses not only more sustainable but also economically viable in high-latitude regions. Thus, glass greenhouses are becoming the preferred platform for next-generation horticulture, which drives their accelerated adoption because of their capacity to host advanced automation, AI-driven crop monitoring, and integrated water recycling.

By Product Insights

The edibles segment held the largest share of 35.6% of the Europe greenhouse horticulture market in 2024. The dominance of the edible segment is majorly attributed to the rising consumer demand for fresh, off-season vegetables and herbs, particularly tomatoes, cucumbers, bell peppers, and leafy greens. Greenhouse cultivation ensures a consistent supply and quality, addressing seasonal gaps in open-field agriculture. According to the study, a portion of tomatoes consumed in Germany and the UK during winter months originates from heated greenhouses, primarily in the Netherlands and Spain. As per the study, greenhouse-grown vegetables exhibit lower pesticide residues than field-grown counterparts, supporting consumer trust. Apart from these, retail chains have committed to sourcing a portion of their fresh produce from protected cultivation, which further strengthens the edibles segment’s market dominance. The expansion of high-wire hydroponic systems, which maximize yield and resource efficiency, is a pivotal driver of this edible segment of the regional market. Hence, the edibles segment continues to attract investment, innovation, and policy support because urban populations are demanding fresh, local, and sustainable food, which ensures its sustained dominance in the greenhouse horticulture landscape.

The ornamentals segment is estimated to register the fastest CAGR of 10.7% over the forecast period, owing to the rising demand for indoor and urban greening, particularly in response to mental well-being trends and biophilic design principles. As per the research, sales of potted plants and cut flowers in urban households increased. Apart from these, municipal greening initiatives are incorporating greenhouse-grown ornamentals into public spaces, driving institutional procurement. Rapid ascent is the integration of automation and precision propagation technologies, which enables high-volume, year-round production of uniform, disease-free plants, and is also a propellant for the ornamentals segment in the regional market. Therefore, the market benefits from predictable demand cycles as climate-controlled greenhouses ensure perfect flowering timing for key retail periods like Easter and Mother’s Day. These technological and commercial advantages position ornamentals as a high-growth and high-margin segment within greenhouse horticulture.

By Application Insights

In 2024, the greenhouse films segment led the Europe greenhouse horticulture market by occupying 37.5% in the regional market. The widespread reliance on plastic coverings across smallholder and commercial operations, particularly in Southern and Eastern Europe, has significantly contributed to the domination of the greenhouse films segment in the regional market. According to the study, notable tonnes of agricultural films are consumed annually in Spain, a portion of which are used in greenhouse applications. These films are engineered for light diffusion, anti-fog properties, and UV stabilization, directly influencing crop yield and energy efficiency. As per the study, optimized films can increase light transmission, which boosts photosynthesis and reduces supplemental lighting needs. The emergence of biodegradable and recyclable film solutions aligned with EU sustainability mandates is also boosting the rise of the greenhouse films segment in the regional market. These advancements are reducing environmental concerns and regulatory risks, which supports the long-term viability and market dominance of greenhouse films in protected cultivation systems.

The horticulture twines segment is anticipated to witness the fastest CAGR of 11.2% from 2025 to 2033. Factors such as the widespread adoption of high-wire cultivation systems for vining crops such as tomatoes, cucumbers, and peppers, which require durable, UV-resistant twines to support vertical growth, are boosting the expansion of the horticulture twines segment in the regional market. According to the research, a portion of tomato greenhouses in the Netherlands use co-polymer twines that can bear loads per plant, ensuring structural integrity over months-long growing cycles. The German Agricultural Society (DLG) reports that twine-based plant training increases yield uniformity by 20% and reduces labor for manual staking. The development of sustainable and biobased twines made from natural fibers such as jute, sisal, and bio-polyethylene is an additional factor surging the growth of the horticulture twines segment in the regional market.

COUNTRY-LEVEL ANALYSIS

Netherlands Greenhouse Horticulture Market Analysis

The Netherlands was the largest region in Europe’s greenhouse horticulture market in 2024 and captured a 32.5% share of the regional market in i024. The domination of the Netherlands in the regional market is primarily driven by its unparalleled concentration of high-tech glasshouses, particularly in the Westland and Oost-Nederland regions, where hectares operate under fully automated climate control. Dutch greenhouses produce notable tonnes of vegetables annually, with tomatoes and bell peppers dominating exports. The Dutch government’s program has facilitated geothermal heating for a portion of the greenhouse area, drastically reducing natural gas dependency. This integration of innovation, policy, and infrastructure strengthens the Netherlands as the continent’s horticultural epicenter.

Spain Greenhouse Horticulture Market Analysis

Spain is closely following in the Europe greenhouse horticulture market with 18% of the regional market share in 2024. Its vast expanse of plastic-covered cultivation in the southeastern provinces of Almería and Murcia is mainly accelerating the expansion of Spain in the regional market. According to the study, notable hectares of plastic greenhouses produce tonnes of vegetables annually, supplying a portion of the EU’s winter tomatoes and cucumbers. The region’s arid climate and abundant sunlight enable near-year-round production with minimal heating. As per the study, drip irrigation and shade nets have reduced water usage. However, concerns over groundwater over-extraction persist.

Italy Greenhouse Horticulture Market Analysis

Italy has experienced steady growth in the Europe greenhouse horticulture market, with a strong focus on Mediterranean crops such as cherry tomatoes, eggplants, and zucchini. As per research, Italy’s agricultural observatory, greenhouse vegetable production reached notable tonnes. The country benefits from favorable solar radiation and proximity to high-demand markets in Central Europe. According to a study, greenhouse farms use integrated pest management (IPM), reducing chemical pesticide use. Apart from these, the Made in Italy brand enhances export value, with premium greenhouse produce commanding higher prices in Germany and Switzerland.

Germany Greenhouse Horticulture Market Analysis

Germany is expanding gradually in the Europe greenhouse horticulture market due to its emphasis on sustainability, automation, and urban integration. According to the study, hectares of glass and plastic greenhouses produce vegetables, herbs, and ornamentals, with Berlin and Bavaria emerging as innovation hubs. The country’s strict environmental regulations have accelerated the shift toward geothermal and district heating. In addition, a portion of German greenhouse gas emissions came from renewable sources, as per research. Urban farms are deploying modular greenhouses in supermarkets and city centers, which shortens supply chains. Therefore, Germany is shaping the future of sustainable and tech-driven horticulture due to strong R&D investment and consumer preference for eco-labeled produce.

France Greenhouse Horticulture Market Analysis

France is expected to be a major player in the European greenhouse horticulture market owing to a balanced mix of vegetable and ornamental production, particularly in the Provence-Alpes-Côte d’Azur and Rhône-Alpes regions. As per the study, greenhouse output reached notable tonnes, with tomatoes, lettuce, and cut flowers as primary crops. The country’s diverse climate allows for regional specialization; Mediterranean zones focus on vegetables, while cooler northern areas cultivate ornamentals. Apart from these, France leads in agrivoltaic greenhouses. Thus, France maintains a resilient and evolving presence in Europe’s protected horticulture landscape because of strong domestic demand and export potential to neighboring countries.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the key players of the Europe greenhouse horticulture market are Richel Group, Hoogendoorn Growth Management B V, Certhon Inc, Dalsem Horticulture Projects B V, HortiMaX B V, Harnois Greenhouses, Priva B V, Ceres Greenhouse Solutions, Certhon, Van Der Hoeven, Oritech Solutions, Netafim Ltd, Ridder Holding Harderwijk B V, Rough Brothers Inc, Top Greenhouses Ltd.

Top Players In The Market

Rijk Zwaan (Netherlands)

Rijk Zwaan is a globally recognized breeder and supplier of vegetable seeds tailored for greenhouse cultivation, with a strong emphasis on disease resistance, yield optimization, and flavor profiling. The company has developed proprietary tomato, pepper, and cucumber varieties specifically adapted to high-wire hydroponic systems prevalent in modern glasshouses. The company operates many international breeding stations. Rijk Zwaan also collaborates with greenhouse operators across Asia-Pacific, providing technical support and seed solutions for controlled-environment farms, which strengthens its role as a knowledge-intensive innovator in sustainable horticulture.

Signify (Netherlands)

Signify, formerly Philips Lighting, has emerged as a pivotal enabler of advanced greenhouse horticulture through its specialized horticultural LED lighting systems. The company’s Philips GreenPower LED interlighting and top lighting solutions are widely deployed in Northern European glasshouses to extend photoperiods and enhance photosynthetic efficiency during low-light months. The company has partnered with major greenhouse clusters in Denmark and Germany to integrate lighting with climate control systems. Its focus on data-driven light recipes and sustainability aligns with global trends toward climate-smart production, strengthening its position as a technology leader in the sector.

Priva (Netherlands)

Priva specializes in climate and process automation systems for greenhouse horticulture, offering integrated control solutions that manage heating, ventilation, irrigation, and energy flows. Its computerized systems are installed in hectares of greenhouses worldwide, enabling precise environmental regulation and resource optimization. Priva also expanded its advisory services to greenhouse operators in China and Japan, providing remote monitoring and AI-assisted decision support. Priva is shaping the digital transformation of horticulture by combining hardware, software, and agronomic expertise, which enhances operational efficiency and sustainability across both European and Asia-Pacific markets.

Top Strategies Used By Key Market Participants

Key players in the Europe greenhouse horticulture market are leveraging technological integration, sustainability-driven innovation, strategic partnerships, geographic expansion, and digitalization to consolidate their competitive advantage. Companies are investing in AI-powered climate control, precision irrigation, and spectral lighting to enhance yield and resource efficiency. Sustainability initiatives include renewable energy integration, biodegradable materials, and closed-loop water systems to comply with EU environmental regulations. Strategic collaborations with research institutions and agri-tech startups accelerate product development and field validation. Expansion into urban and peri-urban farming models strengthens proximity to end markets. Digital platforms offering real-time monitoring, predictive analytics, and remote management are increasingly central to service offerings, enabling growers to optimize performance and reduce operational risks in an energy-constrained and labor-scarce environment.

COMPETITION OVERVIEW

The competition in the Europe greenhouse horticulture market is marked by a convergence of traditional growers, technology providers, and agri-innovation firms, creating a dynamic and highly specialized ecosystem. Incumbent producers compete on yield efficiency, sustainability credentials, and supply chain integration, while technology companies drive differentiation through automation, data analytics, and energy optimization. The Netherlands dominates as a hub of innovation, exporting both physical infrastructure and intellectual capital. Regional players in Southern Europe focus on cost-effective plastic greenhouse production, whereas Northern operators emphasize high-tech glasshouse systems. New entrants, including urban farming startups and vertical agriculture ventures, are redefining production models. Regulatory burdens, energy volatility, and consumer demand for transparency further intensify competition, which compels firms to adopt integrated, resilient, and forward-looking strategies to maintain relevance in a rapidly evolving landscape.

MARKET SEGMENTATION

This research report on the europe greenhouse horticulture market is segmented and sub-segmented into the following categories.

By Covering Material

- Plastic Greenhouse

- Glass Greenhouse

By Product

By Application

- Greenhouse Films

- Grow Bags

- Windbreak And Shelter Nets

- Horticulture Twines

- Other Applications

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe